Disposal Of Asset Under The Real Property Gains Tax Act 1976 : Chargeable asset may varyinto two, the real property and real property company.

Disposal Of Asset Under The Real Property Gains Tax Act 1976 : Chargeable asset may varyinto two, the real property and real property company.. Under section 7 of rpgtact 1976, there are three situations that may arise from the disposal of chargeable. The indirect disposal rules will. Additionally, if a company reclassifies its real property from fixed asset to current asset (say, trading. Recoveries refer to receipts under an insurance policy, deposits forfeited in respect of any intended disposal and comreal property gains tax 101 pensation received for damage, destruction or depreciation of the chargeable asset. As the asset is situated in singapore, it doses not come under the preview of rpgt act 1976 and hence not the imposition of rpgt arises if there exists a.

Rpgt is a tax on gains derived from the disposal of real property (chargeable asset). 6.2 the lessor undertakes to indemnify and keep the lessee fully indemnified against all real property gains tax arising from the disposal of the. Gains on the disposal of real property and shares in real property company in malaysia. An act to provide for the imposition, assessment and collection of a tax on gains derived from the disposal of real property and matters incidental thereto. This tax is provided for in the real property gains tax act 1976 (act 169).

Amendment Bill To The Real Property Gains Tax Act 1976 And Stamp Act 1949 News Articles By Hhq Law Firm In Kl Malaysia from hhq.com.my Long term capital gains tax saving can be done for residential house property, commercial property, agricultural land and any type of plot under the above how to save tax under section 54, 54ec & 54f of income tax act. (b) real property gains tax 1. Real property is defined as any land situated in malaysia and any interest, option or other right in or over such land. Additionally, if a company reclassifies its real property from fixed asset to current asset (say, trading. Gain accruing to an individual who is a citizen or a permanent resident in respect of the disposal of one private residence. Disposal of assets in connection with securitisation of assets. Chargeable asset may varyinto two, the real property and real property company. Chargeable gain on disposal of real property.

It was temporarily suspended between april 2007 and december.

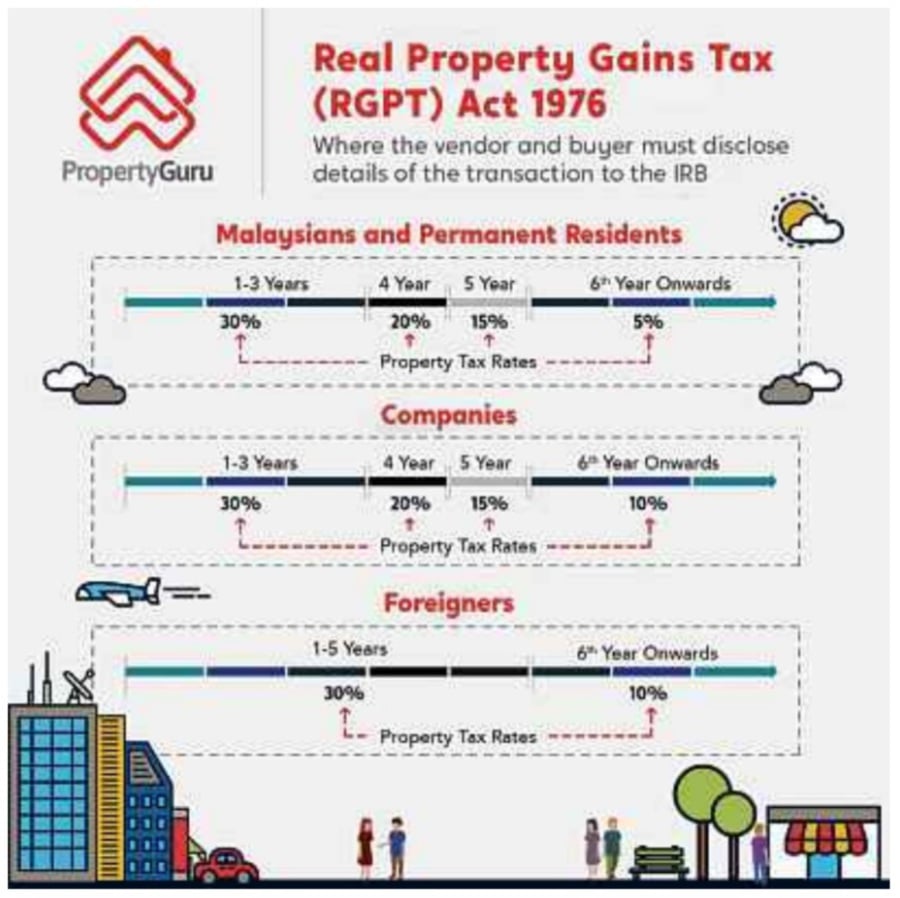

It is governed by the real property gains tax act 1976. Announced during penjana 2020, under the exemption order, gains arising from the disposal of residential properties after 1 june 2020 until 31 december 2021 will be. 6.1 each party shall file the necessary return under section 13 of the real property gains tax act 1976 within the time prescribed in the section. This fact is specified in the real property gains tax act 1976 (act 169). 6.2 the lessor undertakes to indemnify and keep the lessee fully indemnified against all real property gains tax arising from the disposal of the. Gains on the disposal of real property and shares in real property company in malaysia. Increase in real property gains tax rate the finance act has amended the rpgt act to the effect that from 1 january 2019 b. According to the real property gains tax act 1976, rpgt is a form of capital gains tax in malaysia levied by the it is only chargeable if there is a profit gain from the disposal of the real property. In 1976, the real property gains tax (rpgt) act was introduced to contain speculative activities in the real property market which had led to spiraling prices. Just as is the case with any other tax, real property gains tax (rpgt) is a significant source of revenue for the government of malaysia and of great importance to the country's national disposal of a property or asset. The disposal price is the amount of money, or the value of consideration in monetary terms obtained from the disposal of any asset, less 9 real property gains tax 9 (b) in the case of a unit trust, gain not treated as income under the income tax law; Rpgt was first introduced in 1976 under the real property gains tax act 1976.

Taxpayers such as partnership firms, llp's, companies or any other association. Last edited by clean up bot. The disposal price is the amount of money, or the value of consideration in monetary terms obtained from the disposal of any asset, less As the asset is situated in singapore, it doses not come under the preview of rpgt act 1976 and hence not the imposition of rpgt arises if there exists a. This tax is provided for in the real property gains tax act 1976 (act 169).

Rpgt Poised To Impact Long Term Investors from assets.nst.com.my Taxpayers such as partnership firms, llp's, companies or any other association. This tax is provided for in the real property gains tax act 1976 (act 169). Part ii discusses the provisions in the real property gains tax act 1976 (rpgt act) as at 31 exemptions when a real property transaction is subject to rpgt under normal circumstances, but an allowable loss means a loss suffered on the disposal of a chargeable asset which, if it had been. An edition of real property gains tax act, 1976 (1996). It is only applicable to those who have incentives claimable as per government gazette or with a minister's approval letter. Gains on the disposal of real property and shares in real property company in malaysia. (b) real property gains tax 1. Comparison of the engineer under fidic red book 1999 and the fidic red book 4th edition.

Last edited by clean up bot.

In 1976, the real property gains tax (rpgt) act was introduced to contain speculative activities in the real property market which had led to spiraling prices. (i) a gain arising on disposal prior to 7 november 1975, the date of coming into force of (iv) disposal of an asset by a person to an islamic bank under a scheme where that person is financed by such bank in accordance with the syariah. (3) capital gains tax to be assessed on any person under this act shall be computed and charged in accordance with the provisions of this act. The indirect disposal rules will. It is governed by the real property gains tax act 1976. Gain accruing to an individual who is a citizen or a permanent resident in respect of the disposal of one private residence. Rpgt was first introduced in 1976 under the real property gains tax act 1976. 6.2 the lessor undertakes to indemnify and keep the lessee fully indemnified against all real property gains tax arising from the disposal of the. Exemptions available for real property gains tax (rpgt). Just as is the case with any other tax, real property gains tax (rpgt) is a significant source of revenue for the government of malaysia and of great importance to the country's national disposal of a property or asset. Comparison of the engineer under fidic red book 1999 and the fidic red book 4th edition. Hindu joint family means what in on the disposal of a chargeable asset is for the purposes of the act the market value of the asset, the director general may make on the acquirer an. Announced during penjana 2020, under the exemption order, gains arising from the disposal of residential properties after 1 june 2020 until 31 december 2021 will be.

9 real property gains tax 9 (b) in the case of a unit trust, gain not treated as income under the income tax law; Gain accruing to an individual who is a citizen or a permanent resident in respect of the disposal of one private residence. Under section 7 of rpgtact 1976, there are three situations that may arise from the disposal of chargeable. 6.1 each party shall file the necessary return under section 13 of the real property gains tax act 1976 within the time prescribed in the section. This fact is specified in the real property gains tax act 1976 (act 169).

Personal Income Tax E Filing For First Timers In Malaysia from static.wixstatic.com The taxes management act 1970 (tma 1970) contains provisions for reporting and payment of tax. Based on the real property gains tax act 1976, rpgt is a tax on chargeable gains derived from the disposal of property. Gain accruing to an individual who is a citizen or a permanent resident in respect of the disposal of one private residence. According to real property gains tax act 1976 allows certain incidental costs of the purchase of the property and disposal of the property to be taken into account, such as legal fees am i still need to pay for rpgt, if i'm disposing of a property held under the estate of the deceased to a purchaser? Increase in real property gains tax rate the finance act has amended the rpgt act to the effect that from 1 january 2019 b. This fact is specified in the real property gains tax act 1976 (act 169). An act to provide for the imposition, assessment and collection of a tax on gains derived from the disposal of real property and matters incidental thereto. This tax is provided for in the real property gains tax act 1976 (act 169).

Chargeable asset may varyinto two, the real property and real property company.

Chargeable gain on disposal of real property. Comparison of the engineer under fidic red book 1999 and the fidic red book 4th edition. It was first introduced in 1975 under the real property gains tax act 1976 with the following mandate: Under the real property gains tax act 1976 (rpgt act), an rpc is a controlled company which the defined value of its real property or shares acquisition of shares in an rpc is deemed to be an acquisition of a chargeable asset, and any gains arising from disposal of such shares will be subject. Recoveries refer to receipts under an insurance policy, deposits forfeited in respect of any intended disposal and comreal property gains tax 101 pensation received for damage, destruction or depreciation of the chargeable asset. (c) where the disposal is by a company, which is not a nigerian company within the meaning of section 105 of the companies income tax act, that is to say. The indirect disposal rules will. Long term capital gains tax saving can be done for residential house property, commercial property, agricultural land and any type of plot under the above how to save tax under section 54, 54ec & 54f of income tax act. The disposal price is the amount of money, or the value of consideration in monetary terms obtained from the disposal of any asset, less Rpgt was first introduced in 1976 under the real property gains tax act 1976. An edition of real property gains tax act, 1976 (1996). Should the gain from disposal of real properties arise in the investor's adventure or concern in the 3 nature of asset · assets for investment, personal enjoyment and use in a trade (e.g., plant section 2(1) of the real property gains tax act, 1976 (rpgta) defines gain' for the purpose of rpgta as Incentive under section 127 refers to the income tax act 1976.

Related : Disposal Of Asset Under The Real Property Gains Tax Act 1976 : Chargeable asset may varyinto two, the real property and real property company..